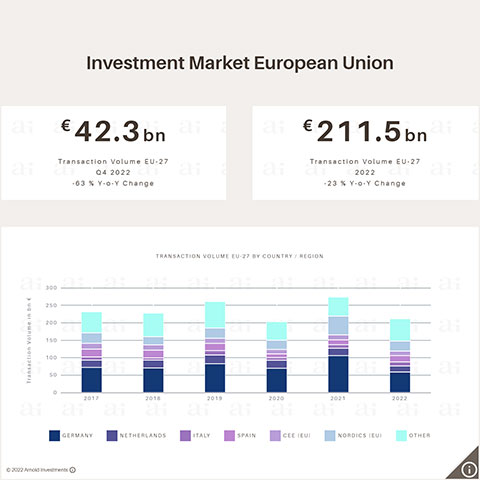

Vienna, 17th of November 2023 - In the third quarter of 2023, the European Union investment market exhibited restrained performance, registering a transaction volume of €23 billion which, in turn, represents a noteworthy year-on-year decline of 57%. The cumulative transaction volume for the initial three quarters of 2023 amounted to approximately €80.4 billion, with domestic investors accounting for 53% of these transactions. Markus Arnold, the CEO and sole proprietor of Arnold Investments, observes "a sustained trend where equity strong private investors continue to be highly active". The leading asset class on the European investment market remained to be office with a transaction volume of €24.3 billion, comprising 30% of the total, followed by residential properties (€16.5 billion; 21%) and retail properties (€14 billion; 17%).

So far this year, a decline of approximately 50% or more has been observed across all major asset classes and primary markets in the real estate sector. A notable exception to this trend are hotel properties which, driven by significant large-scale and portfolio transactions in Southern Europe and France, experienced a year-on-year increase of 12% during the initial three quarters.

Demand for hand-picked existing properties

"In periods characterized by subdued market dynamics, there is a notable demand for selectively chosen existing properties, as well as properties with significant appreciation potential, commonly referred to as 'value-add properties'," ascertains Markus Arnold. This shift in investors’ focus is attributable to the elevated prime yields observed across Europe, reaching levels that present considerable challenges for developers of new properties.

Yield trends in detail

In the third quarter of 2023, there was a notable acceleration in repricing across Europe. The Western European core markets, particularly Germany and the Netherlands, are currently shaping the trajectory of further price developments. Specifically, German office properties in the top 7 cities experienced a substantial increase in prime yields, rising by 45 basis points to 4.55% in Q3 2023. Class A office properties in decentralized locations within the top 7 cities have been achieving yields of approximately 5.65%, marking a quarter-on-quarter increase of 50 basis points. Amsterdam experienced a 50 basis point rise in prime yields for office properties, reaching 4.80% in Q3. In comparison to the historic lows observed in the first quarter of 2022, prime office yields in Germany and the Netherlands have already increased by approximately 1.9 percentage points, while the EU-12 average remains at a modest +1.5 percentage points.

Prime yields have demonstrated sustained upward momentum across all asset classes. The prevailing average prime yields in the EU investment markets under scrutiny currently stand at approximately 4.20% for residential properties (+95 basis points year-on-year), 5.05% for logistics (+90 basis points year-on-year), and roughly 4.65% for high street retail (+85 basis points year-on-year). Remarkably, owing to a distinctly steadier demand, the increase in prime yields for hotel properties was the least pronounced, registering at approximately 70 basis points year-on-year (EU-12: 5.55%).

Opportunities for long-term investments

For the fourth quarter of 2023, an additional rise in prime yields is to be assumed, though this is likely to change in 2024. "The confirmation of the interest rate plateau by the ECB last week is poised to generate growing momentum in the EU investment markets in 2024," affirms Martin Ofner, Head of Market Analysis at Arnold Investments.

Due to the interest rate plateau being reached, and in conjunction with significantly more appealing yield levels, Arnold Investments anticipates an inaugural revitalization of the investment market commencing in early 2024, particularly within the non-core sector.

Given the significantly reduced purchase prices currently prevailing, there exists a substantial spectrum of potential upside for investors with an investment horizon extending beyond five years. This can be attributed to the upward trajectory of rental rates, the anticipated appreciation of capital values and falling costs of financing in the long term.