Berlin, 9 March 2023 - The real estate investment market in Germany shrank by around 44 per cent in 2022 compared to the previous year, says a current market analysis conducted by Arnold Investments. At around EUR 10.2 billion, the investment volume in the fourth quarter 2022 was even 81 per cent lower than in the comparative quarter 2021, whereby this marked an absolute record with EUR 54.9 billion. “The decline in the fourth quarter affects all asset classes with the exception of hotel properties, which are showing a clear increase”, explains Jochen Maurer, Country Manager for Germany at Arnold Investments, a brokerage company operating across Europe. “The declining investment activity has accelerated the repricing process, which is already leading to greater investor interest again this year due to the new yield levels.”

EU-wide downward trend of investment activity

The year of 2022 brought a fundamental change in the market environment for real estate investments. On the one hand, the financing costs have risen considerably, and on the other, competing forms of investment have gained significant market appeal. Yields on 10-year government bonds are now more than 3 percentage points higher than a year ago. German Bunds amount to around 2.6 per cent, UK Gilts and US Treasuries at around 3.9 per cent, respectively. As an immediate result, adjustments of net initial yield levels have taken place across Europe in Q4 2022.

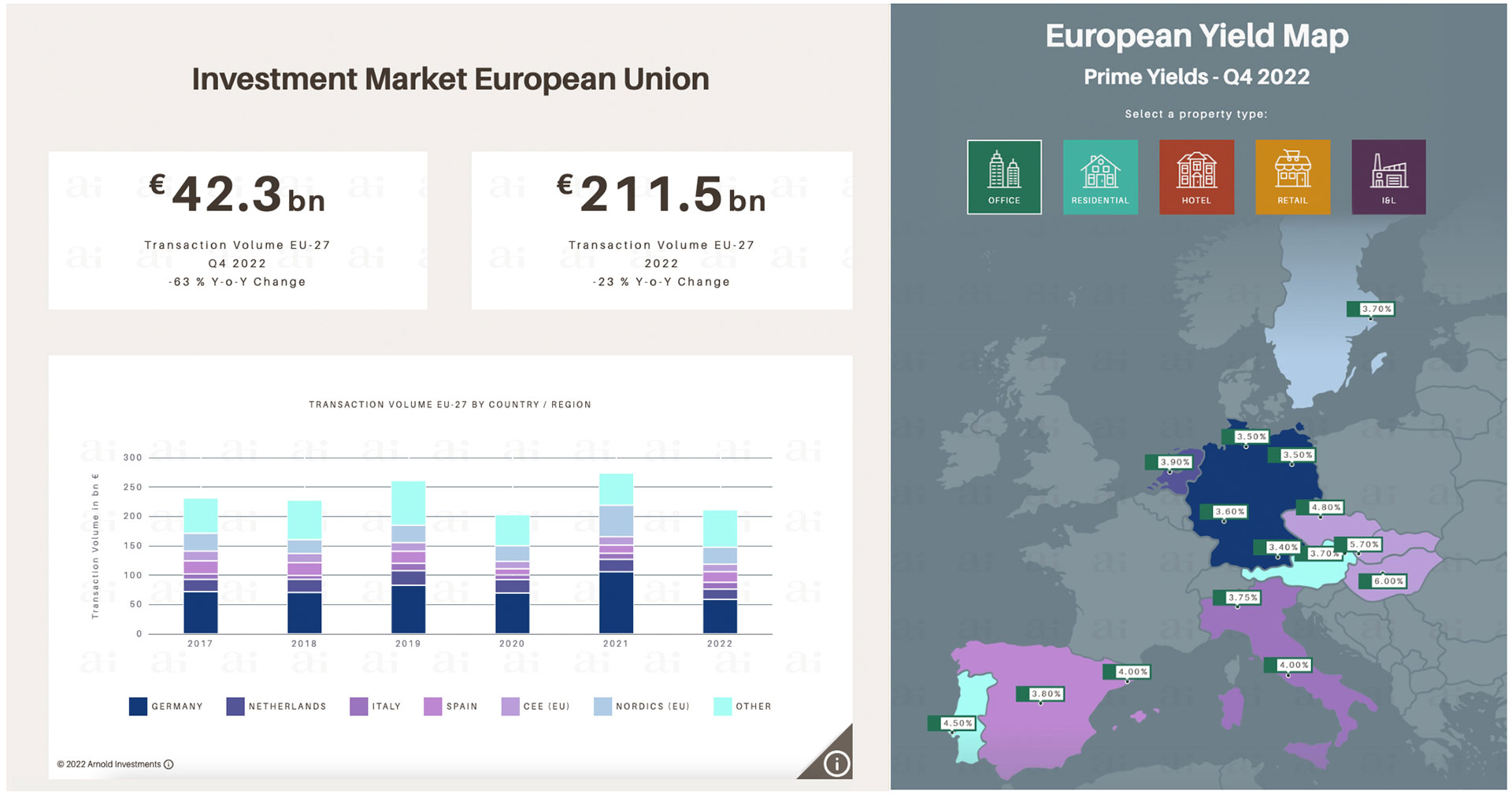

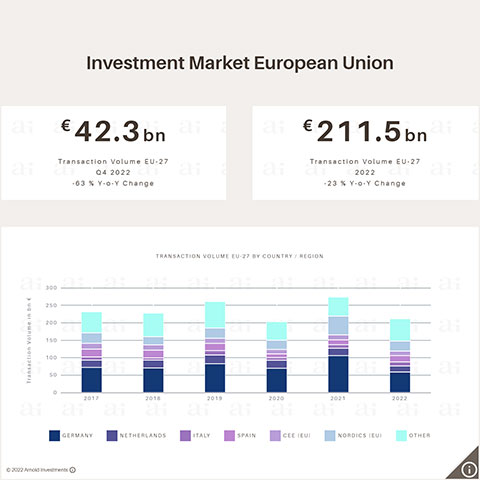

At minus 23 per cent and a total investment volume of EUR 211.5 billion in 2022, the decline in the European Union is somewhat less pronounced than in Germany. However, investment activity throughout the EU also slowed sharply over the course of the year. At around EUR 42.3 billion, the fourth quarter transaction volume was around 63 per cent lower than in the same quarter of 2021. “Although the market activity was extraordinarily high in the comparative period, too”, reports Martin Ofner, Head of Market Analysis at Arnold Investments and responsible for the EU-wide market surveys.

Southern Europe benefits

In 2022, investors have clearly shifted their focus towards the southern European real estate markets. Spain, Portugal as well as Italy – all markets with own branches of Arnold Investments – were able to increase investment volumes in the past year, in some cases significantly.

Overall, the Southern European real estate markets, and particularly those on the the Iberian Peninsula, have benefited from better economic fundamentals since the start of the Russia-Ukraine war due to less dependence on Russian energy supplies. In the industrial sector in particular, competitive advantages have relocated from Germany, Austria and the CEE countries towards Southern Europe. “The extent to which this trend will continue in 2023 will be revealed at the largest international real estate fair, MIPIM in Cannes, where we are represented with our own stand”, says Maurer.

EU investment volume in detail

While all other asset classes recorded a negative development in investment volume over the year, the investment volume in retail real estate rose by 18 per cent to around EUR 29.1 billion in 2022 on EU level. The most significant declines were recorded in the area of medium to large-volume residential investments at minus 52 per cent, which means that this asset class currently represents only around 20 per cent of the overall market. The European hotel investment market was also comparatively stable with a slight decline of 6 per cent to a total volume of EUR 10.6 billion against the previous year. Hotel properties are the only asset class that was able to record a considerable increase in transaction volume in the fourth quarter of 2022 compared to both Q4 2021 and Q3 2022.

In line with the longer-lasting demand in Southern Europe over the course of the year, yields in Spain, Italy and Portugal rose to a lesser extent than in Western Europe up to the end of the year. Using the example of prime yields for CBD office properties, we have registered an increase by around 60 basis points in Southern Europe over the course of 2022, whereas in Germany and the Netherlands an increase by already around 100 basis points occured.

Outlook 2023

Further increases in yields are expected in most European markets and real estate sectors, with a certain proportion attributable to the generally higher rent level due to annual indexations.

Based on the new, higher yield levels, it can be assumed that there will be significantly more attractive investment opportunities on the market in the first half of 2023.